The philosopher George Santayana said: “Those who do not learn from history are doomed to repeat it”. Today, this adage seems increasingly true of defined benefit pension schemes; despite the hundreds of millions of pounds paid by way of sponsor contributions and the suite of asset de-risking strategies deployed each year, deficits continue to rise.

It’s now time for corporate sponsors across the UK to collectively learn from history and acknowledge that the strategy of increasing assets to meet liabilities simply hasn’t worked. The millions of pounds spent on investment de-risking have unquestionably helped improve funding levels but have failed to rein in rising liabilities.

Recent research by JLT Employee Benefits on UK defined benefit schemes indicates that, despite contributions of over £160bn paid in the last 10 years, the total deficit of UK corporate pension schemes has almost doubled to over £900bn and this does not include those schemes which have fallen into the PPF such as BHS and Carillion.

Finance directors across the UK need to act now to rebalance this equation and seek other ways of bringing liabilities back into equilibrium with scheme assets. Executive teams commission significant work to identify, respond to and mitigate risks across their businesses. However, despite the scale risk now inherent in looming deficits, this proactive risk management does not always carry across into the strategy surrounding DB pension liabilities.

In the current economic climate, we are witnessing increasing deficits on company balance sheets impacting dividend payments and banking covenants. The pensions regulator is questioning dividend payments and other corporate transactions in scenarios where there is a pension deficit, which can be an unwelcome hurdle to a company’s commercial objectives.

A smaller pension liability with reduced financial volatility will:

- Improve future cash flows by reducing the period over which deficit contributions are paid

- Improve the net assets and shareholder funds

- Minimise the time spent in explaining fluctuations in financial statements.

Many organisations are taking action to ensure their deficit reduction contributions work harder. Rather than pay contributions solely to increase the assets, finance directors are increasingly channelling their contributions into reducing liabilities, tackling risk and off-setting future cash requirements.

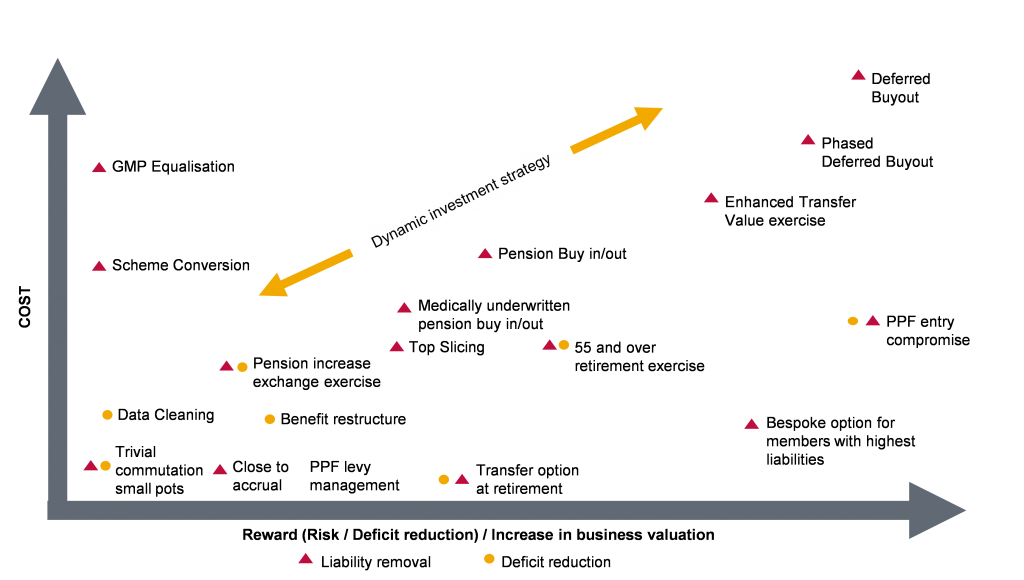

The ultimate objective is for most schemes to wind-up the scheme in a cost effective and structured way. The development of a risk management path will help achieve this without incurring high costs. The chart below identifies a wide range of de-risking tools currently available to finance directors.

Cost-reward relationship of de-risking solutions for consideration

Source JLT Employee Benefits

At a recent seminar series run by JLT, more than 150 trustees and finance directors were asked how they would manage additional company contributions over a three-year period. In the first year, 40% chose to spend the money on a liability reduction exercise, 25% spent it on an LDI investment strategy and the remainder agreed to leave it in the business. Nobody wanted it just paid into the scheme, as the other alternatives provided a greater return without introducing risk. This pattern was repeated in years 2 and 3 with only 1% of attendees proposing additional contributions to the scheme.

These results broadly reflect what is happening in practice; in many schemes, investment strategies have been put in place and finance directors should now be looking at how future deficit contributions can be re-directed to fund member choice exercises.

Reducing liabilities

This is really a question of giving members more options on how they take their benefits, complementing the government’s freedom and choice initiative. Defined benefit scheme pensions are archaic, inflexible and difficult for members to understand; all schemes provide an increasing pension along with benefits on death, which are expensive to both fund and administer. More importantly, however, this benefit pathway may not necessarily fulfil what members want or need in retirement.

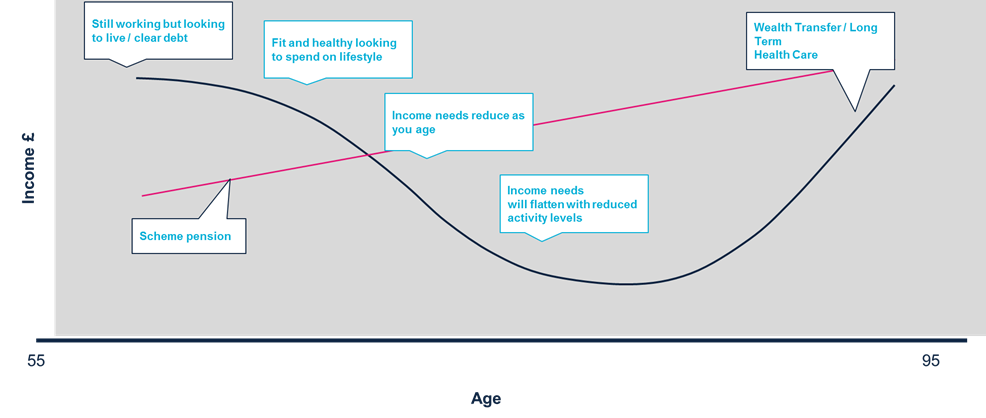

Longer life expectancy does not necessarily mean a longer active life and in many cases, income needs fall as people get older and become less mobile, before rising again to meet ongoing or end-of-life care costs. In light of this, a pension that continues to increase through retirement may not necessarily correlate with members’ needs. Higher levels of income are often required in the earlier years of retirement.

Source JLT Employee Benefits

Common options considered are:

· Pension increase exchange

Offering deferred members (at the point of retirement) and current pensioner members the option to exchange non-statutory pension increases for a higher non-increasing pension. For deferred members, this also increases the lump sum the member can take free of tax. Our research shows that 1 in 3 pensioners accept the offer of a higher current pension in exchange for lower future increases.

· Flexibility at retirement

Providing deferred members aged 55 and over with a quotation of their options to access their pension now. This includes details of the pension available as well as quoting a transfer value (potentially enhanced) and providing access to advice should the member wish to discuss their options. Additionally, from our experience, 1 in 5 deferred members transfer their benefits out of the scheme to access a more flexible retirement income when offered a transfer value instead of a scheme pension.

Such exercises provide the finance director with a smaller scheme, smaller deficit, lower future risks and reduced risk of further contributions in future. All whilst at the same time providing the member with greater choice.

Finance directors can use the previously agreed contributions to put in place a process that includes financial advice, allows members to access their retirement needs and options to make a decision unique to them.

Additionally, FDs should be taking specialised advice now and developing a business plan for the DB scheme consistent with their corporate strategy. They should be discussing with trustees how deficit contributions are actually used and how they can be used to generate a better return whilst at the same time provide additional choice for members

If you think your scheme provides the right retirement income for your members, try asking them about their income needs and what they would prefer. You could be surprised and most importantly the cost of providing what they want could be a lot less than the cost you are currently meeting.

Was this article helpful?

YesNo