Time to cash in on the recent pension funding improvements?

Opportunities are available for companies to take advantage of a benign environment when it comes to defined benefit schemes, says consultants Barnett Waddingham.

Opportunities are available for companies to take advantage of a benign environment when it comes to defined benefit schemes, says consultants Barnett Waddingham.

For the first time in a number of years, financial markets have been kind to companies sponsoring defined benefit (DB) pension schemes.

The aggregate deficit of the FTSE350 DB pension schemes fell from £62bn at the end of 2016 to around £35bn at the end of June this year. This is undoubtedly positive news for DB pension scheme sponsors, according to Nick Griggs, head of corporate consulting at Barnett Waddingham, and companies should now be thinking of managing the huge amount of risk that remains on the table.

Barnett Waddingham’s annual review of the FTSE350 DB schemes highlights some of the trends in the market and the actions that companies should be considering.

One area where companies can take positive action is in relation to the DB scheme investment strategy. While responsibility for the strategy ultimately lies with the trustees of the scheme, it is such an important issue that companies are now taking a more proactive role to ensure that their views are reflected and that they are working collaboratively with the trustees to set an investment strategy that is acceptable to both parties.

There has been a clear trend in the UK of de-risking DB scheme investment strategies – the overall allocation of the FTSE350 DB scheme investments to “growth” assets (i.e. equity, property, etc.) fell from 52% in 2009 to 35% in 2017. Despite this trend, a number of companies are still exposed to a significant amount of risk through their DB scheme investment strategies – 12 FTSE350 companies had an equity holding in their DB scheme that was more than a third of the market capitalisation of the company.

It is important for companies to note that de-risking the DB scheme’s investment strategy does not necessarily mean settling for a lower expected investment return. Pension schemes are increasingly using financial instruments that allow investment risk, particularly the exposure to long-term bond yields, to be reduced while maintaining the expected rate of return. These options are undoubtedly worth exploring for DB pension scheme sponsors.

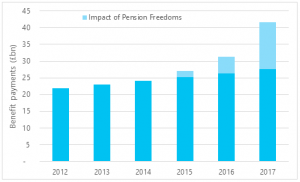

Other areas that should be on the agenda for DB pension scheme sponsors are member engagement strategies and controls put in place for members transferring their benefits out of DB schemes. The chart below shows the level of the benefit payments made from FTSE350 DB schemes over 2017:

This clearly illustrates the impact that George Osborne’s “Pension Freedoms” has had since being introduced in 2015. Despite the “Pension Freedoms” only applying to Defined Contribution (DC) schemes, the impact on DB schemes has been clear. Around £14bn of member benefits were transferred from DB schemes to DC schemes in 2017, as members have moved to access their benefits in a more flexible manner.

From a company perspective, if a member transfers from DB to DC, this will generally result in an improvement in the funding level of the DB scheme (particularly compared to the cost of buying out member benefits with an insurance company), and the risks associated to the provision of the member’s DB benefits are entirely removed. It is therefore in the interest of companies to engage with members so they understand their options and support those who may want to transfer their benefits to a DC scheme.

Companies should be considering how the various benefit options are being communicated to members. This might be at the point of retirement (many companies are now offering a transfer value quotation at retirement as standard), or as a one-off exercise targeted at a particular group of members. It is becoming increasingly popular for companies to provide members with paid-for independent financial advice – not only does this ensure that members are receiving the best possible advice in relation to their benefits, but it also increases the overall volume of members deciding to transfer away from the DB scheme.

Out of the FTSE350 companies, Barclays led the way in terms of transfer volumes in 2017, with £4.2bn being paid out as transfer values from its DB scheme. Aviva, Lloyds Banking Group and Royal Bank of Scotland also saw a significant increase in the level of benefits being paid out.

Finally, for those companies wanting to entirely remove the risk of running their DB scheme, an insurance market transaction is a primary option. While the cost of buying out a DB scheme is generally very high, the recent improvements in funding levels might have made this a more feasible option for a number of schemes.

At the end of 2017, Barnett Waddingham estimated that 29 of the FTSE350 companies could have afforded to buy out their DB scheme with the increase in their cash holdings over the previous year alone, although the consultancy appreciates there will be competing pressures for this money. Since then, funding levels have improved further and annuity pricing has fallen (with pensioner pricing being particularly attractive at present), so for any companies wanting to exit DB pension provision, this option is definitely worth exploring.